Two Key Reasons the Housing Market Won’t Crash in 2024

With ongoing discussions about the economy and concerns of a possible recession, it’s natural for some to worry about a potential housing market crash. However, there’s no reason to panic—the current market conditions are vastly different from those that led to the 2008 housing crisis. Here are two strong reasons why the housing market is unlikely to crash anytime soon.

1. Housing Demand Far Exceeds Supply

One of the leading causes of the 2008 housing crash was an oversupply of homes. But today, the situation is quite different. The current demand for homes far outweighs the available supply, creating a seller’s market.

In a balanced market, there’s typically a six-month supply of homes available for sale. A higher number indicates an oversupply, while a lower number means that demand is outpacing supply. According to recent data from the National Association of Realtors (NAR), we’re currently sitting at just 4.2 months of housing supply—well below the threshold of a balanced market.

Here’s how today compares to past periods:

Before the 2008 crash, there were 13 months of housing supply.

A balanced market has six months of supply.

In 2024, we have only 4.2 months of supply.

This limited supply continues to support home prices, reducing the likelihood of a market crash. While inventory levels vary by location, most regions are experiencing a shortage of homes for sale, keeping prices stable or on the rise.

As Lawrence Yun, Chief Economist at NAR, points out:

"We simply don’t have enough inventory. Some markets may see slight price declines, but a 30% drop in home prices like we saw in 2008 is highly unlikely."

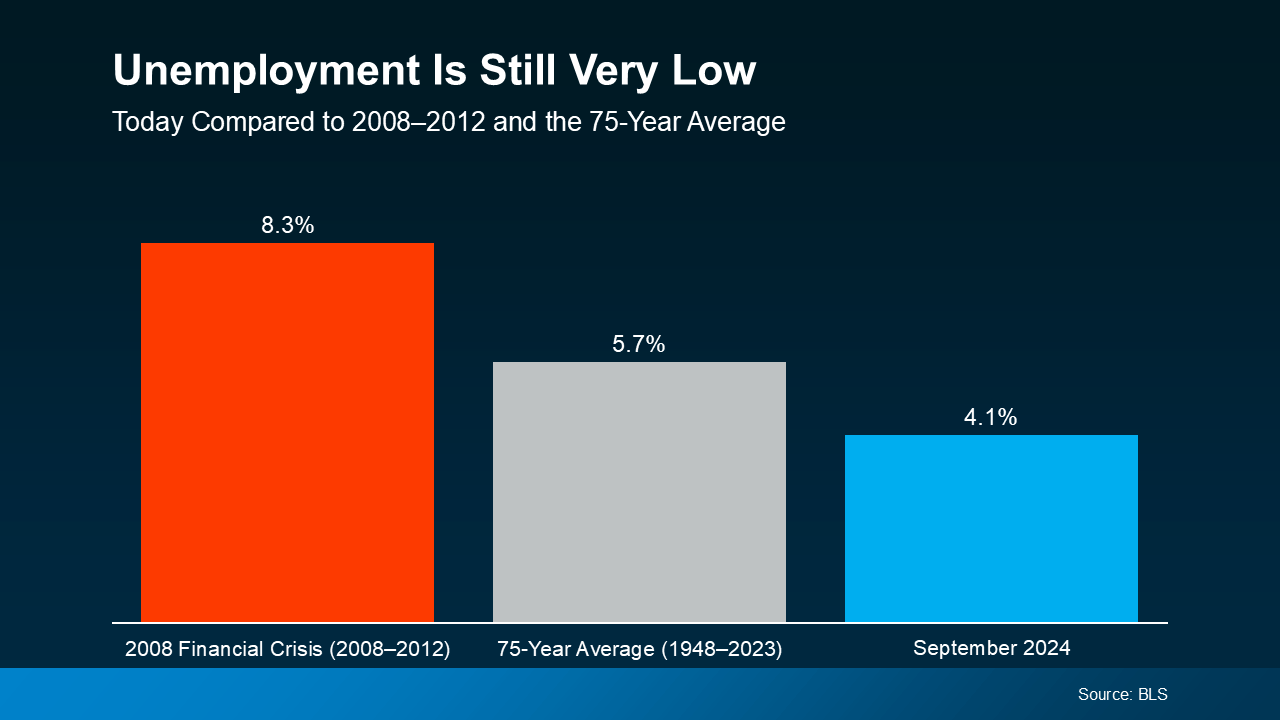

2. Unemployment Remains Low

Another major factor that contributed to the 2008 crash was skyrocketing unemployment. High unemployment led to many homeowners defaulting on their mortgages, resulting in widespread foreclosures. However, the employment landscape today is much healthier.

Current unemployment sits at just 4.1%, compared to 8.3% during the height of the 2008 crisis. With more people employed and earning stable incomes, the risk of mass foreclosures is much lower. Employed homeowners are able to keep up with their mortgage payments, and many are even in a position to buy homes, further boosting demand.

According to the latest data:

2008 financial crisis: 8.3% unemployment

75-year average: 5.7% unemployment

2024 unemployment: 4.1%

The combination of low unemployment and high demand for homes is key to maintaining stability in the housing market.

Today’s Housing Market is Stronger Than in 2008

While concerns about the economy are understandable, it’s important to remember that today’s housing market is fundamentally stronger than it was in 2008. As Rick Sharga, Founder and CEO at CJ Patrick Company, puts it:

"Everything is different about today’s housing market compared to the conditions that led to the 2008 crisis."

With demand still exceeding supply and low unemployment, the housing market is positioned to remain stable for the foreseeable future.

Bottom Line

Although fears of a housing market crash persist, the current conditions suggest otherwise. The key factors driving the market—high demand and low unemployment—are keeping it strong. However, real estate trends can vary by region. If you have questions about the housing market in our area or want personalized advice, feel free to reach out for more insights.